Building a diversified investment portfolio is one of the most effective ways to grow your wealth while minimizing risk. Whether you’re a beginner or an experienced investor, diversification is key to achieving long-term financial success. In this guide, we’ll walk you through the steps to create a well-balanced portfolio that aligns with your goals and risk tolerance.

What Is a Diversified Investment Portfolio?

A diversified portfolio is a collection of different types of investments (stocks, bonds, real estate, etc.) designed to reduce risk and maximize returns. The idea is simple: don’t put all your eggs in one basket. By spreading your investments across various asset classes, industries, and geographic regions, you can protect yourself from market volatility and take advantage of growth opportunities.

Why Diversification Matters

Diversification is often called the “only free lunch in investing” because it allows you to reduce risk without sacrificing returns. Here’s why it’s so important:

Reduces Risk: If one investment performs poorly, others may perform well, balancing out your losses.

Smooths Returns: Diversification helps stabilize your portfolio during market ups and downs.

Maximizes Opportunities: By investing in different areas, you can capitalize on growth in various sectors and regions.

Step-by-Step Guide to Building a Diversified Portfolio

Follow these steps to create a portfolio that’s tailored to your financial goals and risk tolerance.

Step 1: Define Your Financial Goals

Before you start investing, it’s important to know what you’re investing for. Common goals include:

Retirement: Building a nest egg for your golden years.

Buying a Home: Saving for a down payment.

Education: Funding your child’s college education.

Wealth Building: Growing your net worth over time.

Your goals will determine your investment strategy, including your time horizon and risk tolerance.

Step 2: Assess Your Risk Tolerance

Risk tolerance refers to your ability and willingness to withstand market fluctuations. Ask yourself:

How comfortable are you with losing money in the short term for potential long-term gains?

How soon will you need to access your investments?

Pro Tip: Younger investors can typically afford to take more risks, while those nearing retirement may prefer safer investments.

Step 3: Choose Your Asset Allocation

Asset allocation is the process of dividing your investments among different asset classes, such as:

Stocks: High growth potential but higher risk.

Bonds: Lower risk and steady income.

Real Estate: Tangible assets that provide diversification.

Cash/Cash Equivalents: Low risk and high liquidity.

A common rule of thumb is the “100 minus age” rule:

Subtract your age from 100 to determine the percentage of your portfolio to allocate to stocks. The rest can go to bonds and other assets.

Example: If you’re 30 years old, you might allocate 70% to stocks and 30% to bonds.

Step 4: Diversify Within Asset Classes

Once you’ve chosen your asset allocation, diversify within each class:

Stocks: Invest in different industries (tech, healthcare, energy) and geographic regions (U.S., international, emerging markets).

Bonds: Mix government bonds, corporate bonds, and municipal bonds.

Real Estate: Consider REITs (Real Estate Investment Trusts) or rental properties.

Alternative Investments: Explore options like commodities, cryptocurrencies, or peer-to-peer lending.

Step 5: Choose Your Investment Vehicles

There are several ways to build a diversified portfolio:

Index Funds and ETFs: Low-cost, diversified funds that track market indices.

Mutual Funds: Professionally managed funds that pool money from multiple investors.

Individual Stocks and Bonds: For more hands-on investors.

Robo-Advisors: Automated platforms that create and manage a diversified portfolio for you.

Pro Tip: Index funds and ETFs are great for beginners because they offer instant diversification at a low cost.

Step 6: Rebalance Your Portfolio Regularly

Over time, your portfolio’s asset allocation may drift due to market performance. Rebalancing involves adjusting your investments to maintain your desired allocation. For example:

If stocks have grown to 80% of your portfolio (up from 70%), sell some stocks and buy bonds to return to your target allocation.

Pro Tip: Rebalance annually or whenever your allocation deviates significantly from your target.

Common Mistakes to Avoid

Over-Diversification: Spreading your investments too thin can dilute your returns.

Ignoring Fees: High fees can eat into your returns. Choose low-cost investment options.

Emotional Investing: Avoid making decisions based on fear or greed. Stick to your plan.

Tools and Resources to Build Your Portfolio

Here are some tools and resources to help you get started:

Building a diversified investment portfolio is one of the smartest moves you can make for your financial future. By spreading your investments across different asset classes, industries, and regions, you can reduce risk and maximize returns. Remember, the key to success is consistency—start small, stay disciplined, and let your portfolio grow over time.

Ready to take the next step? Use this [Portfolio Allocation Tool] to create your personalized investment plan, and check out our guide on [How to Build Wealth: 10 Timeless Strategies for Financial Freedom] to learn more about creating a secure financial future.

Have you ever heard the saying, “Money makes money, and the money that money makes, makes more money”? That’s the magic of compound interest—one of the most powerful tools for building wealth. Whether you’re saving for retirement, a down payment on a house, or your child’s education, understanding compound interest can help you grow your money exponentially. Let’s break it down.

What Is Compound Interest?

Compound interest is the process of earning interest on both your initial investment (the principal) and the interest that accumulates over time. In simple terms, it’s “interest on interest.” The longer your money compounds, the faster it grows.

Example: If you invest 1,000atanannualinterestrateof71,000atanannualinterestrateof770 in interest after the first year. In the second year, you’ll earn interest on 1,070,notjusttheoriginal1,070,notjusttheoriginal1,000. Over time, this snowball effect can turn small investments into significant wealth.

Why Compound Interest Is So Powerful

The power of compound interest lies in two key factors: time and consistency. Here’s why:

Time: The earlier you start investing, the more time your money has to grow. Even small amounts can turn into substantial sums over decades.

Example: If you invest 200amonthstartingatage25,witha7200amonthstartingatage25,witha7500,000 by age 65. If you start at 35, you’ll only have about $250,000.

Consistency: Regularly adding to your investments amplifies the effects of compounding. Even small contributions can make a big difference over time.

How to Harness the Power of Compound Interest

Ready to put compound interest to work for you? Here’s how to get started:

1. Start Early

The earlier you start investing, the more time your money has to grow. Even if you can only invest a small amount, start now. As the saying goes, “The best time to plant a tree was 20 years ago. The second-best time is now.”

2. Be Consistent

Set up automatic contributions to your investment accounts. Whether it’s 50or50or500 a month, consistency is key to maximizing compound interest.

3. Reinvest Your Earnings

Instead of withdrawing your investment gains, reinvest them to take full advantage of compounding. This is especially important for dividend-paying stocks or interest-bearing accounts.

4. Choose the Right Investment Vehicles

Not all investments are created equal. Look for options with compound growth potential, such as:

Index Funds: Low-cost, diversified investments that track the market.

High-Yield Savings Accounts: Earn interest on your savings with minimal risk.

Retirement Accounts: Take advantage of tax-deferred growth in accounts like 401(k)s or IRAs.

5. Avoid Withdrawing Early

Withdrawing money from your investments interrupts the compounding process. Let your money grow undisturbed for as long as possible.

Real-Life Examples of Compound Interest

Let’s look at two scenarios to illustrate the power of compound interest:

The Early Starter:

Age 25: Starts investing $200 a month with a 7% annual return.

Age 65: Has over $500,000.

The Late Starter:

Age 35: Starts investing $200 a month with the same return.

Age 65: Has about $250,000.

The difference? A 10-year head start nearly doubles the final amount. That’s the power of time and compound interest.

Tools to Calculate Your Compound Interest

Want to see how much your money could grow? Use these tools:

Diversification: Spread your investments to minimize risk. Learn more in our post on [How to Build a Diversified Investment Portfolio].

Conclusion

Compound interest is a simple yet incredibly powerful tool for building wealth. By starting early, staying consistent, and reinvesting your earnings, you can turn small investments into life-changing sums. Remember, the key to success is time—so start today, even if it’s with a small amount.

Ready to take the next step? Use this [Compound Interest Calculator] to see how much your money could grow, and check out our guide on [How to Build Wealth: 10 Timeless Strategies for Financial Freedom] to learn more about creating a secure financial future.

Living on a tight budget doesn’t mean sacrificing your quality of life. In fact, many people who adopt strategic saving techniques find themselves living more comfortably and with less financial stress. With rising inflation and the increasing cost of living, it’s more important than ever to get creative and proactive about saving money.

The key to saving money on a tight budget is to leverage free resources, make smarter spending decisions, and cut back on unnecessary expenses. By implementing these strategies, you can stretch your income further, reduce financial stress, and even build long-term financial security. Below are 10 practical and actionable ways to save money that anyone can apply today.

Many people overlook the free or low-cost services available in their community, which can significantly cut expenses on essentials like food, transportation, healthcare, and entertainment. Whether you’re trying to cut down on grocery bills or find free educational resources, local services can make a big impact on your budget.

How to Implement It

Access Free Food Programs

Food banks and pantries provide free groceries to individuals and families in need. Visit sites like Feeding America to find local food assistance programs.

Some churches and nonprofit organizations host free meal programs for those struggling with food insecurity.

Use Public Libraries

Libraries offer more than books—they provide free Wi-Fi, online courses, audiobooks, and movies.

Many libraries offer career and personal development workshops to help improve financial literacy, job readiness, and tech skills.

Take Advantage of Local Community Centers

Many cities have free or low-cost fitness classes, workshops, and family events.

Community centers often provide subsidized childcare services, free tax assistance, and employment resources.

Example: Maria, a single mother, saved over $600 per year by using free tutoring programs at her local library for her children instead of paying for private lessons. She also started attending free financial literacy classes, which helped her improve her budgeting skills.

Way #2: Learn DIY Skills

Why It Helps

Hiring professionals for every small repair or service quickly adds up. Learning to do simple repairs and maintenance tasks yourself can save you hundreds to thousands of dollars per year. Not only does this cut costs, but it also empowers you with practical life skills.

How to Implement It

Master Basic Home Repairs

Learn how to fix a leaky faucet, unclog drains, and patch drywall—common issues that cost between $150–$400 each time you hire a handyman.

Check out YouTube tutorials or attend DIY workshops at hardware stores like Home Depot or Lowe’s.

Learn to Cook at Home

The average American household spends $3,000 per year eating out. Preparing meals at home can cut that cost by over 50%.

Use budget-friendly recipes and meal prep strategies to save time and money.

Develop Clothing Repair and Maintenance Skills

Instead of buying new clothes, learn basic sewing techniques to repair buttons, fix zippers, or tailor items.

Thrift store finds can be upcycled into trendy and stylish outfits, saving hundreds annually.

Example: Jake used to call a plumber for every minor issue, spending $200+ per visit. After taking a free DIY home repair course at his local community center, he fixed a clogged drain himself for just $10 in supplies.

Way #3: Buy Secondhand and Swap

Why It Helps

Buying brand-new items isn’t always necessary. Thrift shopping and swapping allow you to get high-quality products for a fraction of the retail price. This is especially useful for clothing, furniture, electronics, and household items.

How to Implement It

Shop at Thrift Stores and Online Marketplaces

Visit stores like Goodwill, The Salvation Army, and local consignment shops to find gently used items at up to 80% off retail prices.

Use platforms like Facebook Marketplace, OfferUp, and eBay to buy and sell secondhand goods.

Organize or Join a Swap Group

Arrange a clothing swap event with friends or in your local community.

Many Facebook groups exist for free item exchanges, allowing you to trade unwanted goods instead of buying new ones.

Consider Refurbished Electronics

Buying refurbished smartphones, laptops, and appliances from certified retailers can save you 30–60% compared to brand-new models.

Many companies like Apple and Best Buy offer warranty-backed refurbished products, making them a safe and cost-effective alternative.

Example: Ava, a college student, needed a new laptop but didn’t want to spend $1,000. She purchased a refurbished MacBook for $550, which worked just as well as a brand-new one, saving her nearly 50%.

Way #4: Master the Art of Negotiation

Why It Helps

Many people overpay for services and products simply because they don’t negotiate. Whether it’s internet bills, rent, medical expenses, or even retail purchases, negotiating can save you hundreds to thousands of dollars per year. In fact, a survey by Consumer Reports found that 89% of people who tried negotiating their bills successfully got a discount.

How to Implement It

Negotiate Your Bills

Call your internet, phone, and insurance providers to ask for lower rates.

Research competitor prices and use them as leverage when negotiating.

If you’re a long-term customer, ask for loyalty discounts or promotions.

Lower Your Rent

If you’re renting, offer to sign a longer lease or prepay a few months in exchange for a lower rate.

Point out any maintenance issues and suggest a rent reduction in exchange for handling small repairs yourself.

Get Better Prices on Large Purchases

When shopping for furniture, appliances, or electronics, ask if the store can offer a discount.

Many retailers have price-match policies—use them to your advantage.

Example: Jessica called her internet provider after seeing a competitor’s lower price. After a 10-minute phone call, they reduced her monthly bill by $20, saving her $240 per year.

Way #5: Take Advantage of Free Entertainment

Why It Helps

Entertainment expenses can quickly eat into your budget, but there are many ways to have fun for free. Cutting back on paid activities doesn’t mean missing out—it just means being resourceful.

How to Implement It

Attend Free Community Events

Check your city’s event calendar for free concerts, festivals, and outdoor movie nights.

Many museums and cultural centers offer free admission days.

Enjoy the Outdoors

Visit national parks, beaches, and hiking trails for low-cost or free recreation.

Organize picnics, cycling trips, or stargazing nights instead of expensive outings.

Use Free Streaming & Reading Resources

Instead of paying for Netflix or Spotify, use free streaming platforms like Kanopy, Hoopla, or Pluto TV.

Borrow books, audiobooks, and magazines for free from public libraries.

Example: Mike and his family used to spend $60 per weekend on entertainment. By switching to free community events and library resources, they saved over $3,000 per year while still enjoying great activities.

Way #6: Reduce Hidden Fees and Unnecessary Charges

Why It Helps

Banks, credit cards, and service providers often sneak hidden fees into their charges. Without careful tracking, these small fees accumulate over time, leading to hundreds of dollars lost each year.

How to Implement It

Avoid Bank Fees

Choose no-fee checking and savings accounts to eliminate monthly maintenance fees.

Use in-network ATMs to avoid withdrawal fees.

Set up direct deposit to meet minimum balance requirements and avoid penalties.

Eliminate Unused Subscriptions

Review your monthly statements and cancel unused gym memberships, streaming services, or magazine subscriptions.

Use apps like Trim or Rocket Money to track and cancel unwanted subscriptions automatically.

Be Aware of Credit Card Fees

Avoid late fees by setting up automatic payments.

If you carry a balance, transfer your debt to a lower-interest credit card.

Call your bank to request a waiver on annual fees—many companies will offer this to retain customers.

Example: Samantha realized she was paying $15/month in bank fees and $20/month for an unused gym membership. By switching to a no-fee bank account and canceling her gym membership, she saved $420 per year.

Way #7: Optimize Your Food Spending

Why It Helps

Food is one of the biggest expenses for most households, but many people overspend without realizing it. The USDA estimates that the average American household spends $7,000–$10,000 per year on food, with a significant portion going to restaurants, takeout, and food waste.

How to Implement It

Plan Your Meals & Stick to a Grocery List

Meal planning reduces impulse purchases and food waste.

Create a weekly meal plan based on items you already have.

Use grocery store apps for digital coupons and weekly sales.

Buy in Bulk & Use Freezer-Friendly Meals

Purchase rice, beans, pasta, and frozen vegetables in bulk for long-term savings.

Prep batch meals and freeze leftovers to avoid wasting food.

Limit Dining Out & Find Budget-Friendly Alternatives

Instead of eating out, host potluck dinners or try homemade “restaurant-style” meals.

If dining out, opt for happy hour deals, lunch specials, or discount apps like Too Good To Go.

Example: Sarah and her partner used to spend $250 per month on takeout. By meal planning and cooking at home, they cut their monthly food expenses by 40%, saving over $1,000 per year.

Way #8: Utilize Bartering and Local Exchange Networks

Why It Helps

Bartering allows you to trade skills, goods, or services instead of spending money. This ancient practice has seen a resurgence thanks to online and local exchange communities.

How to Implement It

Join Local Barter Networks

Sign up for Facebook barter groups or apps like Bunz.

Offer services like babysitting, tutoring, or home repairs in exchange for other needed services.

Trade Skills Instead of Paying for Services

Instead of paying a handyman, trade your graphic design or marketing skills.

Exchange homegrown vegetables for baked goods, art, or household essentials.

Organize a Swap Event

Host a clothing swap or toy exchange with friends or neighbors.

Join a tool-sharing community instead of buying expensive equipment.

Example: Jake, a freelance photographer, bartered headshots in exchange for car maintenance. This saved him $300 while providing value to both parties.

Way #9: Explore Energy and Water Conservation Strategies

Why It Helps

Energy and water bills add up quickly, but small conservation efforts can lead to substantial savings over time. The U.S. Department of Energy states that the average household spends $2,000 per year on energy bills, yet 25–30% of that is wasted.

How to Implement It

Reduce Electricity Usage

Unplug electronics when not in use to prevent “phantom energy” loss.

Switch to LED light bulbs, which use up to 75% less energy.

Use a smart thermostat to lower heating and cooling costs.

Save Water & Lower Utility Bills

Install low-flow showerheads and faucet aerators.

Fix leaks immediately—a dripping faucet can waste over 3,000 gallons of water per year.

Use a rain barrel to collect water for gardening.

Example: Emily switched to energy-efficient LED lights and set her thermostat to auto-adjust while away from home. She reduced her energy bill by $300 per year.

Way #10: Monetize Your Hobbies and Skills

Why It Helps

Turning your hobbies into extra income streams allows you to boost your budget without taking on a traditional second job.

How to Implement It

Sell Handmade or Digital Products

Open an Etsy shop for crafts, art, or printables.

Create and sell e-books, digital planners, or online courses.

Offer Freelance Services

Use Upwork, Fiverr, or TaskRabbit to offer services like writing, graphic design, or handyman work.

Teach a skill (e.g., music, yoga, coding) through local classes or online platforms.

Rent Out Your Assets

List an extra room on Airbnb or rent out your car on Turo.

Rent out tools, sports equipment, or photography gear via Fat Llama.

Example: Lisa started selling handmade jewelry on Etsy as a side project. Within a year, she earned $5,000 while working on her hobby in her free time.

Conclusion

Saving money on a tight budget isn’t about cutting corners—it’s about making your money work smarter for you. Each of these ten strategies helps you maximize your resources, reduce unnecessary expenses, and build long-term financial security without feeling restricted.

By leveraging free community resources, you can access essential services at no cost. Learning DIY skills allows you to save on home repairs, clothing, and cooking while gaining independence. Buying secondhand and swapping items keeps quality products in your hands for a fraction of the price. Mastering negotiation helps you cut down monthly expenses effortlessly, while free entertainment options allow you to enjoy life without breaking the bank.

Beyond spending wisely, financial freedom also comes from eliminating hidden fees, optimizing food costs, and bartering for services. Conserving energy and water not only lowers your bills but also benefits the environment. Finally, monetizing your hobbies allows you to increase your income while doing what you love, proving that financial stability isn’t just about saving—it’s also about earning smarter.

Small Steps Lead to Big Savings

Each dollar saved is a step toward financial independence. When you implement just a few of these strategies, you’ll start to see a difference in your monthly budget. Over time, these small changes can lead to thousands of dollars in savings per year, giving you more control over your finances and peace of mind.

Take Action Today

Financial security isn’t reserved for the wealthy—it’s built through consistent, mindful choices. Whether you start by negotiating a bill, reducing food waste, or selling a skill online, every action contributes to a more secure financial future.

Which of these strategies will you apply first? Start today, and watch your savings grow! 🚀

Are you constantly struggling with money despite having a budget? You’re not alone! Many people unknowingly make budgeting mistakes that keep them stuck in a cycle of financial stress. The good news? These mistakes are 100% avoidable—and once you fix them, you’ll be on the fast track to getting out of debt and finally taking control of your money.

The fastest way to turn your financial situation around? Get the ultimate guide that teaches you exactly how to organize your budget and eliminate debt! Grab your copy here 👉 Click to Get Your Budgeting Blueprint Now!

If you don’t track your spending, you’ll never know where your money is going. Little expenses add up, leading to budget shortfalls and financial stress. Studies show that people who actively track their expenses save up to 30% more than those who don’t.

How to Fix It

Use a Budgeting App

Leverage technology to monitor your finances effortlessly. Here are some reputable budgeting apps:

YNAB (You Need A Budget): Uses a zero-based budgeting system to ensure every dollar is accounted for, helping you plan ahead and make informed financial decisions.

Mint: A free app that connects to your bank accounts, categorizes transactions, and provides insights into your spending habits. It also offers bill reminders and credit score monitoring.

Goodbudget: Based on the envelope budgeting method, this app helps you allocate funds for different spending categories and manage your finances proactively.

Maintain a Spending Journal

If you prefer a manual approach, record every expense in a notebook or a digital document. Reviewing your spending patterns weekly can highlight areas where you can cut back.

Set Spending Limits

Establish clear budgets for different expense categories such as groceries, entertainment, and transportation. Regularly reviewing these limits ensures you stay on track and make adjustments as needed.

Example: Imagine you grab a $5 coffee every morning before work. That’s $25 a week, or $1,300 a year! Instead, if you make coffee at home, you could save over $1,000 annually—enough to kickstart an emergency fund or invest in your future.

Without an emergency fund, unexpected expenses (medical bills, car repairs) can destroy your budget and lead to debt. The average unexpected expense costs $1,400, and without savings, many people turn to credit cards with high-interest rates.

How to Fix It

Start Small, Then Build Up

Begin with $500-$1,000 as a starter emergency fund.

Gradually increase it to cover 3-6 months of essential living expenses.

Open a Dedicated Emergency Savings Account

Use a high-yield savings account to keep your funds accessible yet separate from daily spending.

Automate monthly deposits to build your emergency fund effortlessly.

Example: Sarah was doing well financially, but when her car unexpectedly broke down, she had no savings and had to rely on a high-interest credit card. If she had an emergency fund, she could have covered the repair without going into debt.

🚀 Struggling to build an emergency fund? The budgeting blueprint shows you EXACTLY how!Start saving today!

Mistake #3: Setting Unrealistic Budgets

Why This Mistake is Costing You Money

Many people set unrealistic budgets that are either too strict or too vague. A budget that’s too restrictive can lead to frustration and burnout, while a budget without clear structure can result in overspending.

How to Fix It

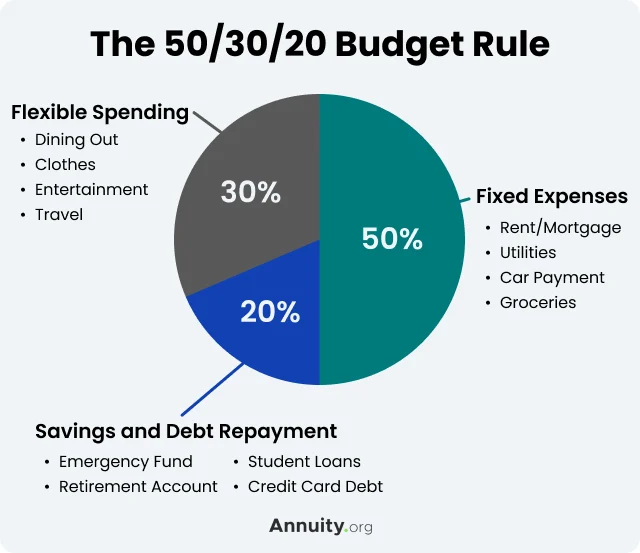

Use the 50/30/20 Rule

A well-balanced budget should account for:

50% of income for necessities (rent, food, bills).

30% for discretionary spending (entertainment, dining out, hobbies).

20% for savings and debt repayment.

Be Flexible & Adjust as Needed

Your budget should evolve with your financial situation. Reassess it monthly to make sure it reflects any changes in income, expenses, or goals.

Example: Emma created an overly strict budget, cutting all entertainment spending. After a month, she felt frustrated and started overspending. Instead, she adjusted her budget to allow for a reasonable entertainment fund, which made it easier to stick to long term.

Mistake #4: Relying on Credit Cards for Everyday Expenses

Why This Mistake is Costing You Money

Using credit cards for daily purchases can lead to high-interest debt, especially if you only pay the minimum balance each month. The average American household carries over $6,000 in credit card debt, with interest piling up rapidly.

How to Fix It

Switch to a Debit or Cash System

Use cash for small, everyday expenses to stay within budget.

Utilize a debit card for essentials instead of relying on credit.

Pay Off Balances in Full

Avoid interest charges by paying off your credit card in full each month. Set up automatic payments to stay on track.

Example: Mike used his credit card for groceries and gas but didn’t pay off his full balance each month. Over a year, he accumulated $800 in interest fees. Switching to a debit card for essentials helped him stay debt-free.

Mistake #5: Forgetting to Adjust Your Budget

Why This Mistake is Costing You Money

Life circumstances change—raises, unexpected expenses, and new financial goals should all prompt budget adjustments. Sticking to an outdated budget can cause unnecessary financial strain.

How to Fix It

Review Your Budget Regularly

Set a monthly budget check-in to evaluate spending and make necessary adjustments.

Reallocate funds based on changing priorities, such as higher savings contributions after a raise.

Account for Seasonal Expenses

Certain months bring extra expenses, like holiday shopping, vacations, or back-to-school costs. Planning ahead prevents financial surprises.

Example: Sarah got a 10% raise but didn’t adjust her budget. Instead of saving more, she unknowingly spent the extra income. After revising her budget, she allocated the raise toward her emergency fund and investment account.

Mistake #6: Overspending on Small Daily Purchases

Why This Mistake is Costing You Money

Many people underestimate the impact of small daily expenses. While a few dollars here and there may seem insignificant, they can add up to thousands of dollars per year, leaving you with less money for savings, investments, or debt repayment.

How to Fix It

Identify Unnecessary Daily Expenses

Track all small purchases for one month to see where your money is going.

Instead of cutting everything, allocate a small, fixed amount for discretionary spending. This prevents impulse purchases while allowing some flexibility.

Example: John used to buy a $10 lunch every workday, spending $200 per month. He started meal prepping at home, cutting his lunch budget to $50 per month—saving $1,800 per year without sacrificing his favorite meals.

Without clear financial goals, you’re more likely to spend aimlessly rather than build wealth. A lack of direction leads to poor financial decisions and delayed financial independence.

How to Fix It

Set SMART Financial Goals

Your goals should be:

Specific – Define exactly what you want (e.g., “Save $10,000 for a house down payment in 12 months”).

Measurable – Track progress over time.

Achievable – Set realistic expectations based on income.

Relevant – Align your goals with your overall financial plan.

Time-bound – Have a clear deadline.

Automate Your Savings

Once you set your goal, make it effortless by setting up automatic transfers to a dedicated savings account.

Example: Emily wanted to build an emergency fund of $5,000 but never got around to saving. She set up an automatic transfer of $200 per month, and within two years, she hit her goal without even thinking about it.

Budgeting isn’t about depriving yourself—it’s about giving yourself more freedom over your money. By avoiding these common mistakes, you set yourself up for financial security, peace of mind, and the ability to enjoy life without constant financial stress.

Here’s what to take away from this guide:

Tracking your spending helps you identify where your money goes, so you can cut waste and spend smarter.

Setting realistic budgets makes it easier to stick with long-term, reducing financial frustration.

Emergency funds prevent financial disasters, saving you from falling into debt during unexpected events.

Credit cards should work for you, not against you—using them wisely avoids costly interest payments.

Your budget should evolve with your life—flexibility is key to staying on track.

Every small expense adds up—but with intentional spending, you can redirect money toward your goals.

Clear financial goals help you build wealth faster—the more specific, the better.

Taking control of your budget doesn’t have to be overwhelming. With the right tools and strategies, you can start making smarter money moves today. If you want a step-by-step plan to master your finances, check out this comprehensive budgeting guide. It provides actionable steps to help you fix budgeting mistakes, eliminate debt, and finally feel confident about your financial future.

Your financial journey starts now. Take that first step toward stress-free finances today!