Building a diversified investment portfolio is one of the most effective ways to grow your wealth while minimizing risk. Whether you’re a beginner or an experienced investor, diversification is key to achieving long-term financial success. In this guide, we’ll walk you through the steps to create a well-balanced portfolio that aligns with your goals and risk tolerance.

What Is a Diversified Investment Portfolio?

A diversified portfolio is a collection of different types of investments (stocks, bonds, real estate, etc.) designed to reduce risk and maximize returns. The idea is simple: don’t put all your eggs in one basket. By spreading your investments across various asset classes, industries, and geographic regions, you can protect yourself from market volatility and take advantage of growth opportunities.

Why Diversification Matters

Diversification is often called the “only free lunch in investing” because it allows you to reduce risk without sacrificing returns. Here’s why it’s so important:

Reduces Risk: If one investment performs poorly, others may perform well, balancing out your losses.

Smooths Returns: Diversification helps stabilize your portfolio during market ups and downs.

Maximizes Opportunities: By investing in different areas, you can capitalize on growth in various sectors and regions.

Step-by-Step Guide to Building a Diversified Portfolio

Follow these steps to create a portfolio that’s tailored to your financial goals and risk tolerance.

Step 1: Define Your Financial Goals

Before you start investing, it’s important to know what you’re investing for. Common goals include:

Retirement: Building a nest egg for your golden years.

Buying a Home: Saving for a down payment.

Education: Funding your child’s college education.

Wealth Building: Growing your net worth over time.

Your goals will determine your investment strategy, including your time horizon and risk tolerance.

Step 2: Assess Your Risk Tolerance

Risk tolerance refers to your ability and willingness to withstand market fluctuations. Ask yourself:

How comfortable are you with losing money in the short term for potential long-term gains?

How soon will you need to access your investments?

Pro Tip: Younger investors can typically afford to take more risks, while those nearing retirement may prefer safer investments.

Step 3: Choose Your Asset Allocation

Asset allocation is the process of dividing your investments among different asset classes, such as:

Stocks: High growth potential but higher risk.

Bonds: Lower risk and steady income.

Real Estate: Tangible assets that provide diversification.

Cash/Cash Equivalents: Low risk and high liquidity.

A common rule of thumb is the “100 minus age” rule:

Subtract your age from 100 to determine the percentage of your portfolio to allocate to stocks. The rest can go to bonds and other assets.

Example: If you’re 30 years old, you might allocate 70% to stocks and 30% to bonds.

Step 4: Diversify Within Asset Classes

Once you’ve chosen your asset allocation, diversify within each class:

Stocks: Invest in different industries (tech, healthcare, energy) and geographic regions (U.S., international, emerging markets).

Bonds: Mix government bonds, corporate bonds, and municipal bonds.

Real Estate: Consider REITs (Real Estate Investment Trusts) or rental properties.

Alternative Investments: Explore options like commodities, cryptocurrencies, or peer-to-peer lending.

Step 5: Choose Your Investment Vehicles

There are several ways to build a diversified portfolio:

Index Funds and ETFs: Low-cost, diversified funds that track market indices.

Mutual Funds: Professionally managed funds that pool money from multiple investors.

Individual Stocks and Bonds: For more hands-on investors.

Robo-Advisors: Automated platforms that create and manage a diversified portfolio for you.

Pro Tip: Index funds and ETFs are great for beginners because they offer instant diversification at a low cost.

Step 6: Rebalance Your Portfolio Regularly

Over time, your portfolio’s asset allocation may drift due to market performance. Rebalancing involves adjusting your investments to maintain your desired allocation. For example:

If stocks have grown to 80% of your portfolio (up from 70%), sell some stocks and buy bonds to return to your target allocation.

Pro Tip: Rebalance annually or whenever your allocation deviates significantly from your target.

Common Mistakes to Avoid

Over-Diversification: Spreading your investments too thin can dilute your returns.

Ignoring Fees: High fees can eat into your returns. Choose low-cost investment options.

Emotional Investing: Avoid making decisions based on fear or greed. Stick to your plan.

Tools and Resources to Build Your Portfolio

Here are some tools and resources to help you get started:

Building a diversified investment portfolio is one of the smartest moves you can make for your financial future. By spreading your investments across different asset classes, industries, and regions, you can reduce risk and maximize returns. Remember, the key to success is consistency—start small, stay disciplined, and let your portfolio grow over time.

Ready to take the next step? Use this [Portfolio Allocation Tool] to create your personalized investment plan, and check out our guide on [How to Build Wealth: 10 Timeless Strategies for Financial Freedom] to learn more about creating a secure financial future.

Have you ever heard the saying, “Money makes money, and the money that money makes, makes more money”? That’s the magic of compound interest—one of the most powerful tools for building wealth. Whether you’re saving for retirement, a down payment on a house, or your child’s education, understanding compound interest can help you grow your money exponentially. Let’s break it down.

What Is Compound Interest?

Compound interest is the process of earning interest on both your initial investment (the principal) and the interest that accumulates over time. In simple terms, it’s “interest on interest.” The longer your money compounds, the faster it grows.

Example: If you invest 1,000atanannualinterestrateof71,000atanannualinterestrateof770 in interest after the first year. In the second year, you’ll earn interest on 1,070,notjusttheoriginal1,070,notjusttheoriginal1,000. Over time, this snowball effect can turn small investments into significant wealth.

Why Compound Interest Is So Powerful

The power of compound interest lies in two key factors: time and consistency. Here’s why:

Time: The earlier you start investing, the more time your money has to grow. Even small amounts can turn into substantial sums over decades.

Example: If you invest 200amonthstartingatage25,witha7200amonthstartingatage25,witha7500,000 by age 65. If you start at 35, you’ll only have about $250,000.

Consistency: Regularly adding to your investments amplifies the effects of compounding. Even small contributions can make a big difference over time.

How to Harness the Power of Compound Interest

Ready to put compound interest to work for you? Here’s how to get started:

1. Start Early

The earlier you start investing, the more time your money has to grow. Even if you can only invest a small amount, start now. As the saying goes, “The best time to plant a tree was 20 years ago. The second-best time is now.”

2. Be Consistent

Set up automatic contributions to your investment accounts. Whether it’s 50or50or500 a month, consistency is key to maximizing compound interest.

3. Reinvest Your Earnings

Instead of withdrawing your investment gains, reinvest them to take full advantage of compounding. This is especially important for dividend-paying stocks or interest-bearing accounts.

4. Choose the Right Investment Vehicles

Not all investments are created equal. Look for options with compound growth potential, such as:

Index Funds: Low-cost, diversified investments that track the market.

High-Yield Savings Accounts: Earn interest on your savings with minimal risk.

Retirement Accounts: Take advantage of tax-deferred growth in accounts like 401(k)s or IRAs.

5. Avoid Withdrawing Early

Withdrawing money from your investments interrupts the compounding process. Let your money grow undisturbed for as long as possible.

Real-Life Examples of Compound Interest

Let’s look at two scenarios to illustrate the power of compound interest:

The Early Starter:

Age 25: Starts investing $200 a month with a 7% annual return.

Age 65: Has over $500,000.

The Late Starter:

Age 35: Starts investing $200 a month with the same return.

Age 65: Has about $250,000.

The difference? A 10-year head start nearly doubles the final amount. That’s the power of time and compound interest.

Tools to Calculate Your Compound Interest

Want to see how much your money could grow? Use these tools:

Diversification: Spread your investments to minimize risk. Learn more in our post on [How to Build a Diversified Investment Portfolio].

Conclusion

Compound interest is a simple yet incredibly powerful tool for building wealth. By starting early, staying consistent, and reinvesting your earnings, you can turn small investments into life-changing sums. Remember, the key to success is time—so start today, even if it’s with a small amount.

Ready to take the next step? Use this [Compound Interest Calculator] to see how much your money could grow, and check out our guide on [How to Build Wealth: 10 Timeless Strategies for Financial Freedom] to learn more about creating a secure financial future.

What if you could achieve financial freedom and live life on your own terms? The truth is, building wealth isn’t just for the lucky few—it’s a skill anyone can master. Whether you’re just starting out or looking to grow your existing wealth, the principles of wealth-building remain the same, no matter the era. In this guide, you’ll learn 10 proven strategies that have stood the test of time and can help you secure your financial future.

Why Building Wealth Matters

Building wealth isn’t just about having more money—it’s about creating opportunities, security, and freedom for yourself and your loved ones. Here’s why it matters:

Security: Life is unpredictable. Building wealth ensures you’re prepared for emergencies, job loss, or unexpected expenses.

Freedom: Financial freedom means having the ability to make choices without being constrained by money. Whether it’s traveling, starting a business, or retiring early, wealth gives you options.

Legacy: Wealth allows you to leave a lasting impact, whether it’s supporting your family, donating to causes you care about, or creating generational wealth.

As Warren Buffett once said, “Do not save what is left after spending, but spend what is left after saving.” This timeless advice underscores the importance of prioritizing wealth-building in your life.

10 Timeless Strategies to Build Wealth

These strategies are tried, tested, and proven to work—no matter when you start. Let’s dive in:

1. Spend Less Than You Earn (The Golden Rule)

The foundation of wealth-building is simple: spend less than you earn. This creates a surplus that you can save, invest, and grow over time. Here’s how to do it:

Track Your Expenses: Use budgeting tools like YNAB or Mint to understand where your money is going.

Cut Unnecessary Costs: Identify areas where you can reduce spending (e.g., dining out, subscriptions).

Live Below Your Means: Avoid lifestyle inflation—just because you earn more doesn’t mean you should spend more.

Pro Tip: Aim to save at least 20% of your income. If that’s not possible, start small and increase over time.

2. Invest Early and Consistently

Time is your greatest ally when it comes to investing. Thanks to compound interest, even small, consistent investments can grow into significant wealth over time. Here’s how to get started:

Start with Index Funds: These low-cost investments track the market and are perfect for beginners.

Automate Your Investments: Set up automatic contributions to your investment accounts to stay consistent.

Think Long-Term: Avoid trying to time the market. Focus on steady, long-term growth.

Example: If you invest 500amonthwithanaverageannualreturnof7500amonthwithanaverageannualreturnof71 million in 30 years.

3. Diversify Your Income Streams

Relying on a single source of income is risky. Diversifying your income not only increases your earning potential but also provides a safety net. Consider:

Side Hustles: Freelancing, consulting, or starting a small business.

Passive Income: Rental properties, dividend stocks, or creating digital products.

Investments: Stocks, bonds, or real estate.

Pro Tip: Start with one additional income stream and scale up as you gain experience.

4. Educate Yourself About Money

Financial literacy is the key to making smart money decisions. Dedicate time to learning about personal finance, investing, and wealth-building. Here are some resources to get started:

Books: The Millionaire Next Door, Rich Dad Poor Dad, The Intelligent Investor.

Podcasts: The Dave Ramsey Show, ChooseFI, BiggerPockets Money.

Courses: Online platforms like Coursera or Udemy offer affordable finance courses.

Remember: Knowledge is power—especially when it comes to money.

5. Avoid Debt and Build an Emergency Fund

Debt can derail your wealth-building efforts, especially high-interest debt like credit cards. Here’s how to stay on track:

Pay Off High-Interest Debt First: Use the debt avalanche or snowball method.

Build an Emergency Fund: Save 3-6 months’ worth of living expenses to cover unexpected costs.

Avoid Lifestyle Debt: Don’t take on debt for non-essentials like luxury items or vacations.

Pro Tip: Treat your emergency fund as a non-negotiable expense.

6. Invest in Yourself (Your Greatest Asset)

Your ability to earn and grow wealth starts with you. Invest in your skills, education, and personal growth to increase your earning potential. Consider:

Learning New Skills: Take courses or certifications in high-demand fields.

Networking: Build relationships with people who can help you grow professionally.

Health and Wellness: A healthy body and mind are essential for long-term success.

Remember: The best investment you can make is in yourself.

7. Take Calculated Risks

Wealth-building often requires stepping out of your comfort zone. However, not all risks are created equal. Here’s how to take smart risks:

Invest in the Stock Market: While there’s risk involved, historically, the market has provided strong returns over time.

Start a Business: If you have a solid plan and the resources, entrepreneurship can be a powerful wealth-building tool.

Avoid Gambling: Speculative investments like cryptocurrency or day trading should only make up a small portion of your portfolio.

Pro Tip: Always do your research and never risk more than you can afford to lose.

8. Think Long-Term

Wealth-building is a marathon, not a sprint. Avoid get-rich-quick schemes and focus on sustainable, long-term strategies. Here’s how:

Set Clear Goals: Define what financial freedom means to you and create a plan to achieve it.

Stay Patient: Don’t get discouraged by short-term setbacks.

Reinvest Your Earnings: Let your money work for you by reinvesting dividends and profits.

Example: If you save 10,000ayearfor20yearswitha710,000ayearfor20yearswitha7400,000.

9. Leverage Tax-Advantaged Accounts

Taxes can take a big bite out of your wealth. Use tax-advantaged accounts to keep more of your money. Consider:

401(k) or IRA: Contribute to retirement accounts to reduce your taxable income.

HSAs: Health Savings Accounts offer triple tax benefits for medical expenses.

529 Plans: Save for education expenses tax-free.

Pro Tip: Maximize your contributions to these accounts to take full advantage of their benefits.

10. Give Back and Practice Gratitude

Wealth isn’t just about accumulating money—it’s also about making a positive impact. Giving back can bring fulfillment and perspective to your wealth-building journey. Consider:

Donating to Charity: Support causes you care about.

Mentoring Others: Share your knowledge and help others succeed.

Practicing Gratitude: Appreciate what you have while striving for more.

Remember: True wealth is about more than just money—it’s about living a meaningful life.

Common Wealth-Building Mistakes to Avoid

Even with the best strategies, it’s easy to make mistakes. Here are some common pitfalls to watch out for:

Overspending: Living beyond your means can sabotage your wealth-building efforts.

Emotional Investing: Making decisions based on fear or greed can lead to poor outcomes.

Neglecting Savings: Failing to save for emergencies or retirement can leave you vulnerable.

Pro Tip: Stay disciplined and stick to your plan, even when it’s challenging.

Tools and Resources to Build Wealth

Here are some tools and resources to help you on your wealth-building journey:

Budgeting Apps: YNAB, Mint, or Personal Capital.

Investment Platforms: Vanguard, Fidelity, or Robinhood.

Books: The Millionaire Next Door, Your Money or Your Life, The Simple Path to Wealth.

Pro Tip: Start with one tool or resource and expand as you grow more comfortable.

Frequently Asked Questions (FAQ)

Q: How much should I save to start building wealth? A: Aim to save at least 20% of your income, but start with whatever you can and increase over time.

Q: What’s the best way to start investing as a beginner? A: Begin with low-cost index funds or robo-advisors to minimize risk and learn the basics.

Q: How long does it take to build wealth? A: Wealth-building is a long-term process. Stay consistent, and you’ll see results over time.

Conclusion

Building wealth is a journey, not a sprint. By following these 10 timeless strategies, you can create a secure financial future and achieve the freedom to live life on your own terms. Start today—your future self will thank you.

Which strategy will you try first? Let us know in the comments below!

Looking to boost your income without quitting your day job? Whether you want extra cash to pay off debt, build savings, or fund a passion project, a side hustle can be your path to financial freedom. The rise of the gig economy has made it easier than ever to earn money on your own schedule, with some side hustlers turning their gigs into full-time businesses.

From freelancing and digital marketing to selling products and renting out assets, there are countless ways to generate extra income. The key is choosing a hustle that fits your skills, interests, and available time while maximizing your earning potential.

In this guide, we’ll break down the most profitable and flexible side hustles, showing you how much you can earn, how to get started, and the best strategies for success. NOTE: This is a long Post – go to the Table of contents and press CTRL + F to search what interest you the most or check the whole content.

Freelancing allows you to monetize your skills by offering services like writing, graphic design, programming, and more. Among these, copywriting is one of the most lucrative and in-demand freelance careers, with businesses constantly seeking skilled writers to create engaging marketing content.

How much can you earn?

Beginner copywriters make around $25-$50 per hour.

Experienced freelancers charge $100-$250 per hour.

Top-tier copywriters earn $10,000+ per project by writing high-converting sales pages and email campaigns.

The average annual salary for freelance copywriters is $74,513, with some making well over six figures.

How to Get Started

1. Develop Your Skills

Study persuasive writing techniques to master the psychology of effective marketing.

Read classic books like The Boron Letters or Scientific Advertising.

Take online courses to sharpen your skills in sales copy, content writing, and direct response marketing.

2. Build a Strong Portfolio

Create sample sales pages, blog posts, or email campaigns to showcase your work.

Offer pro bono or low-cost work to small businesses to gain experience.

Start a personal blog to demonstrate your writing style and attract clients.

3. Find Clients

Use platforms like Upwork, Fiverr, and Freelancer to land your first gigs.

Pitch directly to businesses by sending cold emails to potential clients.

Network on LinkedIn and join freelance writing communities.

4. Set Competitive Rates

Start with a reasonable rate and increase pricing as you gain experience.

Charge per project, per word, or hourly depending on the client’s needs.

Offer retainer packages for long-term clients to ensure steady income.

Boost Your Success with Copywriting Mastery

Want to skyrocket your income as a copywriter? The secret is understanding how to craft words that persuade and sell. If you want to learn the exact techniques top copywriters use to create compelling content, check out The Copywriting Enigma Decoded.

What You’ll Learn in This E-book:

The 3 Primal Drivers behind customer purchasing decisions.

The Covert Indoctrination Formula to hook and convert readers effortlessly.

How to use high-impact words and powerful copywriting formulas.

The psychology behind branding and messaging that sells.

Print-on-demand (POD) is a low-risk, high-reward business model where you sell custom-designed products without holding inventory. With the rise of e-commerce and personalization trends, POD has become a multi-billion-dollar industry, expected to grow at a CAGR of 26.1% between 2023 and 2030 (Grand View Research).

Since there are no upfront costs for inventory, anyone can start a POD business with little to no investment—just a creative vision and marketing strategy.

How Much Can You Earn?

Your earnings depend on the niche, pricing strategy, and marketing efforts. Here’s a breakdown:

Beginners can earn $500–$2,000 per month by selling designs on marketplaces like Redbubble, Teespring, or Spreadshirt.

Intermediate sellers using Shopify with targeted ads can earn $5,000–$10,000+ per month.

Top POD store owners generate six or seven figures annually, scaling with automation and paid advertising.

A report from Printful found that profit margins range between 30-50%, meaning that if you sell a hoodie for $45, you can make $15-$20 per sale.

How to Get Started

1. Choose a Profitable Niche

Niching down helps reduce competition and attract a dedicated customer base.

Some high-converting POD niches include:

Pet lovers (custom pet portraits, funny dog/cat apparel)

If you’re artistic, use software like Adobe Illustrator, Canva, or Procreate to design unique graphics.

If you’re not a designer, you can outsource designs from platforms like Fiverr or Upwork.

3. Select a Print-on-Demand Supplier

Printful, Printify, and SPOD are some of the top POD providers that integrate with Shopify, Etsy, and WooCommerce.

Consider factors like product selection, pricing, and shipping times before choosing your supplier.

4. Set Up Your Online Store

Option 1: Sell on POD marketplaces like Redbubble, Teespring, or Zazzle (easier, but lower profit margins).

Option 2: Build a Shopify or Etsy store to retain control over branding and pricing.

5. Market Your Products

Use social media (Instagram, TikTok, Pinterest) to showcase designs.

Run Facebook and Google Ads to drive targeted traffic to your store.

Leverage influencer marketing—offer free products in exchange for exposure.

Example of a Successful POD Business

Sarah started her POD store selling custom t-shirts for dog lovers. By leveraging Instagram and Facebook ads, she made $15,000 in her first three months. Now, her store generates $50,000+ per month, with most of the process automated using Printful.

Side Hustle #3: Dropshipping

Why It’s Profitable

Dropshipping is a fulfillment method where retailers sell products without holding inventory. Instead of stocking products, when a customer places an order, the retailer purchases the item from a third-party supplier, who then ships it directly to the customer. This eliminates warehouse costs, upfront inventory investments, and the risk of unsold stock.

The global dropshipping market has been expanding rapidly, valued at $365.67 billion in 2024, and is projected to reach $1.25 trillion by 2030, growing at a 22% CAGR (Grand View Research).

Since this business model allows you to start with minimal investment, it has become a popular option for aspiring entrepreneurs looking to enter the e-commerce space.

How Much Can You Earn?

Your dropshipping earnings depend on the products, niche, and marketing efforts you choose. Here’s a breakdown of what’s possible:

Beginners: Many new dropshippers earn between $1,000 to $2,000 per month within the first few months.

Experienced Entrepreneurs: Those who refine their marketing strategy can reach $10,000 to $50,000+ per month.

Top Dropshipping Stores: Some elite dropshippers generate six to seven figures annually by scaling successful product lines.

Profit Margins: Typically range from 20% to 30% per sale, meaning if you sell a product for $50, you can make $10–$15 per sale.

How to Get Started

1. Choose a Profitable Niche

Market Research: Identify trending products with consistent demand by analyzing platforms like Google Trends, TikTok, and Amazon Best Sellers.

Competition Analysis: Avoid overly saturated markets unless you have a unique branding angle.

Pet products (interactive toys, customized collars, feeding solutions)

2. Find Reliable Suppliers

Use platforms like AliExpress, SaleHoo, and CJ Dropshipping to source products.

Consider U.S.-based suppliers for faster shipping and higher-quality products.

Communicate with suppliers to verify reliability, shipping times, and customer service.

3. Set Up an E-commerce Store

Option 1: Use Shopify (most popular for beginners) due to its easy integrations with dropshipping apps.

Option 2: Set up a WooCommerce store if you prefer working with WordPress.

Option 3: Sell through marketplaces like eBay and Amazon for additional traffic sources.

4. Implement a Winning Marketing Strategy

Social Media Ads: Run Facebook, Instagram, and TikTok Ads to drive traffic to your store.

SEO & Content Marketing: Optimize your store for Google searches and write blogs related to your niche.

Influencer Marketing: Partner with TikTok and Instagram influencers to showcase your products.

Email Marketing: Build an email list to retarget customers with promotions and new product launches.

5. Automate Operations & Manage Orders

Use dropshipping apps like Oberlo, Zendrop, or Spocket to streamline fulfillment.

Set up automated email follow-ups for abandoned carts.

Offer great customer service to build brand trust and increase repeat sales.

Example of a Successful Dropshipping Business

Mark, a college student, started a dropshipping store selling eco-friendly water bottles. By leveraging TikTok ads and influencer collaborations, he scaled his store to $20,000/month in sales within six months. Now, he reinvests profits into scaling winning products and expanding his brand.

Want to Master Dropshipping? Learn the Essentials with This Guide!

While dropshipping offers huge profit potential, success requires strategy, research, and execution. If you want to shorten the learning curve and start making money faster, consider getting Dropshipping 101 Audio & eBook.

What You’ll Learn in This Guide:

The exact steps to launching a profitable dropshipping business.

How to find trending products that sell like crazy.

The best platforms and suppliers for sourcing winning products.

Marketing strategies that turn clicks into consistent sales.

Dropshipping offers low-risk, high-reward potential if you choose winning products, build a strong brand, and optimize marketing efforts. The key to success lies in testing multiple products, understanding customer behavior, and continually refining your sales funnel.

Side Hustle #4: Renting Out Assets

Why It’s Profitable

Renting out assets is one of the most effective ways to generate passive income without requiring much effort. Whether you own a spare room, a car, photography equipment, or even storage space, you can monetize these resources and earn consistent revenue.

With the rise of the sharing economy, platforms like Airbnb, Turo, and Neighbor have made it incredibly easy to rent out personal assets. The global vacation rental market alone is projected to reach $107.7 billion by 2027, growing at a CAGR of 5.3% (Statista).

How Much Can You Earn?

Airbnb Rentals: Renting out a spare room or property can earn $1,500–$4,000 per month, depending on the location and demand.

Car Rentals via Turo: Renting your vehicle through Turo can generate $500–$1,500 per month.

Storage Space via Neighbor: If you have unused space, you can make $50–$300 per month renting it out for storage.

Equipment Rentals: High-end cameras, drones, and audio equipment can rent for $50–$200 per day on platforms like Fat Llama.

How to Get Started

1. Identify Assets You Can Rent

Spare rooms or vacation properties → List on Airbnb, Vrbo, or Booking.com.

Vehicles → Rent through Turo or Getaround.

Storage space (garage, basement, attic) → List on Neighbor.

Photography & video gear → Use Fat Llama or ShareGrid.

Power tools, party equipment, camping gear → Rent out locally through Facebook Marketplace or dedicated rental platforms.

2. Optimize Your Listings

Take high-quality photos to make your listing stand out.

Write a compelling description highlighting the features and benefits of your asset.

Set competitive pricing based on location, seasonality, and demand.

Encourage reviews to build trust and increase bookings.

3. Ensure a Smooth Rental Experience

Automate check-ins & check-outs for Airbnb properties using smart locks.

Set clear rental agreements to protect your assets.

Offer excellent customer service—quick responses lead to better reviews and more bookings.

Example of a Successful Rental Business

Lisa, a homeowner in Miami, listed her spare bedroom on Airbnb and quickly started earning $2,500 per month in passive income. She reinvested her earnings into furnishing another unit, scaling her Airbnb business to $8,000 per month within a year.

Want to Start Your Own Rental Business? Learn from the Experts!

The Short-Term Rental Airbnb Arbitrage E-Guidebook provides everything you need to launch and scale a profitable rental business—whether you’re starting with a single room or building an entire portfolio.

📖 What You’ll Learn in This Guide:

The step-by-step process of setting up your rental business.

How to find and negotiate property leases for Airbnb arbitrage.

Optimizing your listings for maximum bookings.

Scaling your business to multiple properties.

Advanced marketing & SEO strategies to increase visibility and bookings.

Renting out assets is an excellent way to generate passive income while leveraging things you already own. Whether you start small or scale into a full-fledged rental business, this side hustle provides steady cash flow with minimal effort.

Side Hustle #5: Social Media Management

Why It’s Profitable

With over 4.9 billion social media users worldwide (Statista), businesses of all sizes need a strong social media presence to engage customers and drive sales. However, most business owners lack the time or expertise to manage their social media accounts effectively, making social media management one of the most in-demand digital skills today.

How Much Can You Earn?

Beginners: Freelance social media managers earn $20–$50 per hour starting out.

Experienced Professionals: Those with proven results can charge $75–$150 per hour.

Monthly Retainers: Many businesses pay $500–$5,000 per month for ongoing social media management.

Full-Time Income: Experienced managers working with multiple clients can easily earn $50,000–$100,000+ per year.

How to Get Started

1. Develop Your Skills

Learn the basics of social media marketing (Instagram, Facebook, LinkedIn, TikTok, Twitter, Pinterest).

Stay updated on content trends, hashtags, and algorithm changes.

Get familiar with tools like Canva (graphic design), Buffer or Hootsuite (scheduling), and Meta Business Suite (analytics).

2. Build a Portfolio

Offer free or discounted services to a local business or entrepreneur to gain experience.

Create case studies showcasing how you increased engagement, followers, or sales for a client.

Post social media tips and success stories on your own social media pages to demonstrate expertise.

3. Find Clients

Use freelance platforms like Upwork, Fiverr, or Freelancer to land your first gigs.

Network on LinkedIn and Facebook groups for business owners.

Offer packages instead of hourly rates—businesses prefer fixed monthly pricing for ongoing work.

4. Offer High-Value Services

Content creation (graphics, captions, video editing, carousel posts).

Community engagement (replying to comments, DMs, customer interactions).

Ad management (Facebook & Instagram Ads, lead generation strategies).

Analytics & reporting (track key metrics to measure success).

Example of a Successful Social Media Manager

Emma, a stay-at-home mom, started managing Instagram and Facebook pages for small businesses in her city. After three months, she secured four clients paying $1,000/month each. Now, she earns $4,000 per month working part-time from home.

Side Hustle #6: Teaching or Tutoring Online

Why It’s Profitable

Online education is booming, with the global e-learning market expected to reach $457.8 billion by 2026 (Statista). As more students and professionals seek to enhance their skills from home, online tutors and educators have seen a massive increase in demand.

Whether you specialize in academic subjects, language tutoring, or professional skills, online teaching can be an extremely profitable and flexible side hustle.

How Much Can You Earn?

Freelance Tutors: Earn $15–$50 per hour depending on experience and subject demand.

ESL (English as a Second Language) Teachers: Typically earn $10–$40 per hour, depending on the platform.

Specialized Skill Instructors (Coding, Business, Music, Test Prep, etc.): Can charge $50–$150 per hour.

Course Creators: Those who create and sell online courses can generate $500–$50,000+ per month, depending on audience size and marketing efforts.

How to Get Started

1. Choose Your Teaching Niche

Academic Subjects: Math, Science, History, English, SAT/ACT/GRE test prep.

Languages: English, Spanish, Mandarin, French, etc.

Professional Skills: Coding, Digital Marketing, Finance, Business Strategy.

Creative Skills: Music, Photography, Video Editing, Graphic Design.

Live Group Classes: OutSchool, Zoom, or personalized coaching.

3. Set Your Pricing & Offer Packages

Research competitor pricing to set competitive rates.

Offer discounts on long-term tutoring packages to secure consistent income.

Bundle pre-recorded lessons or study materials for additional revenue.

4. Market Yourself

Optimize your profile on tutoring platforms with professional credentials and student testimonials.

Create content on social media (e.g., TikTok, YouTube, LinkedIn) to showcase expertise.

Use email marketing to attract repeat students and referrals.

Example of a Successful Online Tutor

Daniel, a former high school teacher, started tutoring SAT and ACT prep online. Within six months, he built a steady client base, earning over $6,000 per month. Eventually, he transitioned into selling test prep courses, scaling his earnings to $20,000 per month.

Online tutoring and teaching provide a flexible, high-paying income stream while allowing you to help others grow their knowledge. Whether you choose one-on-one tutoring, live classes, or course creation, this side hustle has unlimited earning potential.

Side Hustle #7: Affiliate Marketing

Why It’s Profitable

Affiliate marketing is one of the most effective ways to earn passive income by promoting products and earning a commission for each sale made through your referral link. With the global affiliate marketing industry expected to reach $17 billion by 2027 (Statista), this business model has created six-figure and even seven-figure earners who strategically promote high-converting products.

How Much Can You Earn?

Beginners: Can earn $100–$1,000 per month by promoting digital or physical products.

Intermediate Affiliate Marketers: Typically earn $1,000–$10,000 per month through targeted strategies.

Top Affiliate Marketers: Those with large audiences or effective funnels can generate $50,000–$100,000+ per month.

Commission Rates: Typically range from 5% (physical products) to 75% (digital products).

How to Get Started

1. Choose a Niche

Personal Finance & Investing → Promote courses, budgeting apps, and financial products.

Health & Fitness → Promote supplements, workout programs, and fitness gear.

Digital Marketing & Business → Promote software, courses, and business tools.

Tech & Gadgets → Promote high-ticket electronics and gadgets.

2. Sign Up for Affiliate Programs

Amazon Associates → Best for promoting physical products.

ClickBank & Digistore24 → High-commission digital products.

Hotmart → A great platform for online courses and digital products.

ShareASale & CJ Affiliate → Variety of e-commerce and software affiliate programs.

3. Build an Audience & Promote Effectively

Start a Blog → Write SEO-optimized articles that drive organic traffic.

Create a YouTube Channel → Review and recommend affiliate products.

Leverage Social Media → Promote products through Instagram, TikTok, and Pinterest.

Use Email Marketing → Build an email list and nurture subscribers with valuable content.

4. Track & Optimize Performance

Use tracking tools like Google Analytics, Bitly, or Pretty Links to monitor clicks and conversions.

Test different strategies such as split testing landing pages and tweaking ad copy.

Focus on high-converting products that provide value to your audience.

Example of a Successful Affiliate Marketer

Mike started a YouTube channel reviewing tech gadgets and inserted affiliate links in his video descriptions. Within six months, he was making $5,000 per month, and after a year, his earnings exceeded $15,000 per month through consistent content creation and audience growth.

Want to Master Affiliate Marketing? Start Here!

Affiliate marketing is a powerful way to generate passive income, but many beginners struggle with understanding the fundamentals. That’s why the Affiliate Marketing A-Z eBook is the perfect resource to help you get started the right way.

What You’ll Learn in This Guide:

The step-by-step process of launching an affiliate marketing business.

The common mistakes beginners make and how to avoid them.

An A-Z glossary of the most important affiliate marketing terms.

Proven strategies to maximize your commissions and grow your audience.

Affiliate marketing provides endless income potential if you choose the right niche, build trust with your audience, and promote valuable products. Whether you’re looking for a side income or a full-time business, this is one of the best scalable, passive income models available.

Side Hustle #8: Virtual Assistance

Why It’s Profitable

As businesses continue to move online, virtual assistants (VAs) are in higher demand than ever. Entrepreneurs, small business owners, and even large corporations hire VAs to handle administrative, marketing, and customer service tasks, allowing them to focus on business growth.

The global virtual assistant market is projected to grow at a CAGR of 12.3% and reach $25.6 billion by 2028 (GlobeNewswire), making it a lucrative remote work opportunity for anyone with organizational skills.

How Much Can You Earn?

Entry-Level Virtual Assistants: Earn between $15–$30 per hour handling basic admin work.

Specialized VAs (Social Media, E-commerce, Tech Support): Earn $30–$60 per hour.

Executive Virtual Assistants: Charge $75+ per hour for high-level business support.

Full-Time Income Potential: Many experienced VAs earn $3,000–$8,000+ per month, working from home on a flexible schedule.

How to Get Started

1. Identify Your Skills & Services

General Admin Tasks: Email management, scheduling, data entry.

Social Media Management: Content creation, scheduling posts, engagement.

Customer Support: Responding to customer inquiries, handling refunds, live chat assistance.

E-commerce Support: Managing Shopify or Etsy stores, processing orders.

Automation & Productivity: Zapier, Notion, Google Workspace.

Example of a Successful Virtual Assistant

Samantha, a former office assistant, transitioned into full-time virtual assistance specializing in Pinterest marketing for bloggers. Within 8 months, she built a steady client base of 10 businesses, earning over $6,000 per month while working remotely.

Virtual assistance is an ideal side hustle for individuals with strong organizational skills and a passion for helping businesses run smoothly. Whether you choose general admin work, social media management, or e-commerce support, this flexible and remote-friendly job can become a full-time income source.

Side Hustle #9: Pet Sitting and Dog Walking

Why It’s Profitable

With pet ownership on the rise, the demand for pet sitting and dog walking services has skyrocketed. In the U.S. alone, 67% of households own a pet, and the pet care industry is expected to reach $358.62 billion globally by 2027 (Fortune Business Insights). Busy pet owners are constantly looking for reliable caregivers to help with their furry friends, making this a lucrative and enjoyable side hustle.

How Much Can You Earn?

Dog Walkers: Earn $15–$35 per walk, depending on location and duration.

Pet Sitters: Charge $25–$100 per night for overnight stays.

House Sitting with Pets: Earn $1,500–$4,000 per month caring for pets while homeowners are away.

Full-Time Income Potential: Many experienced pet sitters make over $50,000 per year, especially if they build a loyal client base.

How to Get Started

1. Choose Your Services

Dog Walking: Short or long walks, solo or group walks.

Pet Sitting: In-home care, feeding, grooming, playtime.

Overnight Boarding: Taking care of pets in your home.

Specialized Care: Administering medications, senior pet care, puppy training support.

2. Find Clients

Join Pet Service Platforms: Sign up on Rover, Wag!, and Care.com.

Advertise Locally: Post in Facebook groups, Nextdoor, and community bulletin boards.

Create a Website & Social Media Presence: Share testimonials and daily pet updates to attract customers.

3. Build Trust & Increase Bookings

Get Certified: Pet CPR & First Aid certifications increase credibility.

Encourage Reviews: Positive testimonials lead to more referrals.

Offer Discounts for First-Time Clients: This builds initial trust and encourages long-term business.

Example of a Successful Pet Sitter

Lisa, a college student, started dog walking on weekends and quickly built a steady client base. Within six months, she expanded to overnight pet sitting and began earning $3,500 per month—all while setting her own schedule and spending time with animals she loves.

Want to Provide the Best Care for Pets? Learn from the Experts!

If you’re serious about becoming a trusted pet sitter or dog walker, it’s essential to understand pet health, training, and behavioral needs. The Ultimate Dog Care for New Pet Parents course is the perfect resource for anyone looking to care for pets professionally or personally.

📖 What You’ll Learn in This Guide:

The best practices for feeding, training, and grooming dogs.

How to handle behavioral challenges, including excessive barking and anxiety.

Essential pet care routines to keep dogs healthy and happy.

Exclusive bonuses, including 67 homemade dog food recipes and a 7-week dog training guide.

Pet sitting and dog walking offer flexibility, steady income, and the joy of working with animals. Whether you start as a weekend side hustle or turn it into a full-time career, this business can be highly rewarding!

Side Hustle #10: Flipping Items for Profit

Why It’s Profitable

Flipping items for profit—buying undervalued products and reselling them for a higher price—is a proven way to make quick cash. With online marketplaces booming, resellers are making full-time incomes by sourcing products at thrift stores, garage sales, clearance racks, and liquidation sites.

The global resale market is expected to grow to $350 billion by 2027, driven by the increasing popularity of secondhand shopping and sustainable fashion (ThredUp Report). Whether you focus on clothing, electronics, furniture, or collectibles, flipping offers high earning potential with minimal upfront investment.

How Much Can You Earn?

Beginner Flippers: Can earn $500–$2,000 per month flipping thrifted or discounted items.

Part-Time Resellers: Typically make $3,000–$5,000 per month by scaling their inventory and using multiple platforms.

Full-Time Professional Flippers: Those with established strategies can earn $10,000+ per month by sourcing high-value items.

Profit Margins: Most flippers see 100%–500% ROI on certain items, depending on sourcing strategy.

Liquidation Websites: Buy returned or surplus inventory at B-Stock, Liquidation.com, or Direct Liquidation.

Facebook Marketplace & Craigslist: Negotiate for undervalued items locally.

3. List Items for Sale

eBay: Best for collectibles, electronics, and trending products.

Facebook Marketplace & OfferUp: Ideal for local sales, furniture, and appliances.

Poshmark & Depop: Specialize in fashion, shoes, and accessories.

Amazon & Etsy: Perfect for high-demand products or handmade/vintage items.

4. Maximize Profit with Smart Selling Strategies

Take high-quality photos to attract buyers.

Write compelling product descriptions with relevant keywords.

Price competitively based on demand and competitor listings.

Offer bundle deals or discounts for multiple purchases.

Example of a Successful Flipper

John started flipping sneakers as a side hustle, buying limited-edition shoes from retail drops and reselling them for double or triple the price. Within a year, he expanded into electronics and vintage collectibles, scaling his flipping business to $7,000 per month while working from home.

Flipping items for profit is a low-cost, high-reward side hustle that can turn bargain hunting into a serious income stream. Whether you’re looking for a quick side gig or want to scale into a full-fledged business, this hustle allows you to earn on your terms.

Conclusion: Choose Your Path to Extra Income

The journey to financial freedom doesn’t have to be complicated. Whether you want to supplement your income, escape the 9-to-5, or build a full-fledged business, these 10 side hustles offer real earning potential. The key is to take action, stay consistent, and keep learning.

Each hustle has its unique strengths:

Freelancing & Copywriting: Monetize your skills and build a career in digital services.

Print-on-Demand & Dropshipping: Start an e-commerce business with minimal investment.

Rental Arbitrage & Asset Leasing: Generate passive income by utilizing your existing assets.

Social Media Management & Virtual Assistance: Work remotely and earn high hourly rates.

Pet Sitting & Dog Walking: Turn your love for animals into steady income.

Flipping & Reselling: Make quick profits by sourcing undervalued products.

Your All-in-One Resource Hub

To help you kickstart your side hustle, we’ve gathered the best guides and courses to give you step-by-step training in these fields:

📖 Affiliate Marketing A-Z – Master the fundamentals of affiliate marketing. Get it here!

📖 Dropshipping 101 – Learn how to launch a successful dropshipping store. Start now!

📖 The Copywriting Enigma Decoded – Unlock the power of persuasive writing. Claim your copy!

📖 Short-Term Rental & Airbnb Arbitrage Guide – Build a profitable rental business. Get started here!

📖 Ultimate Dog Care for New Pet Parents – Become the best pet sitter with expert insights. Check it out!

💡 Now it’s time to take action! Pick a hustle that excites you, equip yourself with the right knowledge, and start building your extra income stream today. 🚀

FAQ

Q: What is the easiest side hustle to start? A: Freelancing, virtual assistance, and dog walking require little investment.

Q: Can I do a side hustle while working full-time? A: Yes! Many side hustles like affiliate marketing and freelancing can be done in your free time.

Q: How long does it take to make money from a side hustle? A: Some, like freelancing, can start paying in a few weeks, while others take months to grow.

Living on a tight budget doesn’t mean sacrificing your quality of life. In fact, many people who adopt strategic saving techniques find themselves living more comfortably and with less financial stress. With rising inflation and the increasing cost of living, it’s more important than ever to get creative and proactive about saving money.

The key to saving money on a tight budget is to leverage free resources, make smarter spending decisions, and cut back on unnecessary expenses. By implementing these strategies, you can stretch your income further, reduce financial stress, and even build long-term financial security. Below are 10 practical and actionable ways to save money that anyone can apply today.

Many people overlook the free or low-cost services available in their community, which can significantly cut expenses on essentials like food, transportation, healthcare, and entertainment. Whether you’re trying to cut down on grocery bills or find free educational resources, local services can make a big impact on your budget.

How to Implement It

Access Free Food Programs

Food banks and pantries provide free groceries to individuals and families in need. Visit sites like Feeding America to find local food assistance programs.

Some churches and nonprofit organizations host free meal programs for those struggling with food insecurity.

Use Public Libraries

Libraries offer more than books—they provide free Wi-Fi, online courses, audiobooks, and movies.

Many libraries offer career and personal development workshops to help improve financial literacy, job readiness, and tech skills.

Take Advantage of Local Community Centers

Many cities have free or low-cost fitness classes, workshops, and family events.

Community centers often provide subsidized childcare services, free tax assistance, and employment resources.

Example: Maria, a single mother, saved over $600 per year by using free tutoring programs at her local library for her children instead of paying for private lessons. She also started attending free financial literacy classes, which helped her improve her budgeting skills.

Way #2: Learn DIY Skills

Why It Helps

Hiring professionals for every small repair or service quickly adds up. Learning to do simple repairs and maintenance tasks yourself can save you hundreds to thousands of dollars per year. Not only does this cut costs, but it also empowers you with practical life skills.

How to Implement It

Master Basic Home Repairs

Learn how to fix a leaky faucet, unclog drains, and patch drywall—common issues that cost between $150–$400 each time you hire a handyman.

Check out YouTube tutorials or attend DIY workshops at hardware stores like Home Depot or Lowe’s.

Learn to Cook at Home

The average American household spends $3,000 per year eating out. Preparing meals at home can cut that cost by over 50%.

Use budget-friendly recipes and meal prep strategies to save time and money.

Develop Clothing Repair and Maintenance Skills

Instead of buying new clothes, learn basic sewing techniques to repair buttons, fix zippers, or tailor items.

Thrift store finds can be upcycled into trendy and stylish outfits, saving hundreds annually.

Example: Jake used to call a plumber for every minor issue, spending $200+ per visit. After taking a free DIY home repair course at his local community center, he fixed a clogged drain himself for just $10 in supplies.

Way #3: Buy Secondhand and Swap

Why It Helps

Buying brand-new items isn’t always necessary. Thrift shopping and swapping allow you to get high-quality products for a fraction of the retail price. This is especially useful for clothing, furniture, electronics, and household items.

How to Implement It

Shop at Thrift Stores and Online Marketplaces

Visit stores like Goodwill, The Salvation Army, and local consignment shops to find gently used items at up to 80% off retail prices.

Use platforms like Facebook Marketplace, OfferUp, and eBay to buy and sell secondhand goods.

Organize or Join a Swap Group

Arrange a clothing swap event with friends or in your local community.

Many Facebook groups exist for free item exchanges, allowing you to trade unwanted goods instead of buying new ones.

Consider Refurbished Electronics

Buying refurbished smartphones, laptops, and appliances from certified retailers can save you 30–60% compared to brand-new models.

Many companies like Apple and Best Buy offer warranty-backed refurbished products, making them a safe and cost-effective alternative.

Example: Ava, a college student, needed a new laptop but didn’t want to spend $1,000. She purchased a refurbished MacBook for $550, which worked just as well as a brand-new one, saving her nearly 50%.

Way #4: Master the Art of Negotiation

Why It Helps

Many people overpay for services and products simply because they don’t negotiate. Whether it’s internet bills, rent, medical expenses, or even retail purchases, negotiating can save you hundreds to thousands of dollars per year. In fact, a survey by Consumer Reports found that 89% of people who tried negotiating their bills successfully got a discount.

How to Implement It

Negotiate Your Bills

Call your internet, phone, and insurance providers to ask for lower rates.

Research competitor prices and use them as leverage when negotiating.

If you’re a long-term customer, ask for loyalty discounts or promotions.

Lower Your Rent

If you’re renting, offer to sign a longer lease or prepay a few months in exchange for a lower rate.

Point out any maintenance issues and suggest a rent reduction in exchange for handling small repairs yourself.

Get Better Prices on Large Purchases

When shopping for furniture, appliances, or electronics, ask if the store can offer a discount.

Many retailers have price-match policies—use them to your advantage.

Example: Jessica called her internet provider after seeing a competitor’s lower price. After a 10-minute phone call, they reduced her monthly bill by $20, saving her $240 per year.

Way #5: Take Advantage of Free Entertainment

Why It Helps

Entertainment expenses can quickly eat into your budget, but there are many ways to have fun for free. Cutting back on paid activities doesn’t mean missing out—it just means being resourceful.

How to Implement It

Attend Free Community Events

Check your city’s event calendar for free concerts, festivals, and outdoor movie nights.

Many museums and cultural centers offer free admission days.

Enjoy the Outdoors

Visit national parks, beaches, and hiking trails for low-cost or free recreation.

Organize picnics, cycling trips, or stargazing nights instead of expensive outings.

Use Free Streaming & Reading Resources

Instead of paying for Netflix or Spotify, use free streaming platforms like Kanopy, Hoopla, or Pluto TV.

Borrow books, audiobooks, and magazines for free from public libraries.

Example: Mike and his family used to spend $60 per weekend on entertainment. By switching to free community events and library resources, they saved over $3,000 per year while still enjoying great activities.

Way #6: Reduce Hidden Fees and Unnecessary Charges

Why It Helps

Banks, credit cards, and service providers often sneak hidden fees into their charges. Without careful tracking, these small fees accumulate over time, leading to hundreds of dollars lost each year.

How to Implement It

Avoid Bank Fees

Choose no-fee checking and savings accounts to eliminate monthly maintenance fees.

Use in-network ATMs to avoid withdrawal fees.

Set up direct deposit to meet minimum balance requirements and avoid penalties.

Eliminate Unused Subscriptions

Review your monthly statements and cancel unused gym memberships, streaming services, or magazine subscriptions.

Use apps like Trim or Rocket Money to track and cancel unwanted subscriptions automatically.

Be Aware of Credit Card Fees

Avoid late fees by setting up automatic payments.

If you carry a balance, transfer your debt to a lower-interest credit card.

Call your bank to request a waiver on annual fees—many companies will offer this to retain customers.

Example: Samantha realized she was paying $15/month in bank fees and $20/month for an unused gym membership. By switching to a no-fee bank account and canceling her gym membership, she saved $420 per year.

Way #7: Optimize Your Food Spending

Why It Helps

Food is one of the biggest expenses for most households, but many people overspend without realizing it. The USDA estimates that the average American household spends $7,000–$10,000 per year on food, with a significant portion going to restaurants, takeout, and food waste.

How to Implement It

Plan Your Meals & Stick to a Grocery List

Meal planning reduces impulse purchases and food waste.

Create a weekly meal plan based on items you already have.

Use grocery store apps for digital coupons and weekly sales.

Buy in Bulk & Use Freezer-Friendly Meals

Purchase rice, beans, pasta, and frozen vegetables in bulk for long-term savings.

Prep batch meals and freeze leftovers to avoid wasting food.

Limit Dining Out & Find Budget-Friendly Alternatives

Instead of eating out, host potluck dinners or try homemade “restaurant-style” meals.

If dining out, opt for happy hour deals, lunch specials, or discount apps like Too Good To Go.

Example: Sarah and her partner used to spend $250 per month on takeout. By meal planning and cooking at home, they cut their monthly food expenses by 40%, saving over $1,000 per year.

Way #8: Utilize Bartering and Local Exchange Networks

Why It Helps

Bartering allows you to trade skills, goods, or services instead of spending money. This ancient practice has seen a resurgence thanks to online and local exchange communities.

How to Implement It

Join Local Barter Networks

Sign up for Facebook barter groups or apps like Bunz.

Offer services like babysitting, tutoring, or home repairs in exchange for other needed services.

Trade Skills Instead of Paying for Services

Instead of paying a handyman, trade your graphic design or marketing skills.

Exchange homegrown vegetables for baked goods, art, or household essentials.

Organize a Swap Event

Host a clothing swap or toy exchange with friends or neighbors.

Join a tool-sharing community instead of buying expensive equipment.

Example: Jake, a freelance photographer, bartered headshots in exchange for car maintenance. This saved him $300 while providing value to both parties.

Way #9: Explore Energy and Water Conservation Strategies

Why It Helps

Energy and water bills add up quickly, but small conservation efforts can lead to substantial savings over time. The U.S. Department of Energy states that the average household spends $2,000 per year on energy bills, yet 25–30% of that is wasted.

How to Implement It

Reduce Electricity Usage

Unplug electronics when not in use to prevent “phantom energy” loss.

Switch to LED light bulbs, which use up to 75% less energy.

Use a smart thermostat to lower heating and cooling costs.

Save Water & Lower Utility Bills

Install low-flow showerheads and faucet aerators.

Fix leaks immediately—a dripping faucet can waste over 3,000 gallons of water per year.

Use a rain barrel to collect water for gardening.

Example: Emily switched to energy-efficient LED lights and set her thermostat to auto-adjust while away from home. She reduced her energy bill by $300 per year.

Way #10: Monetize Your Hobbies and Skills

Why It Helps

Turning your hobbies into extra income streams allows you to boost your budget without taking on a traditional second job.

How to Implement It

Sell Handmade or Digital Products

Open an Etsy shop for crafts, art, or printables.

Create and sell e-books, digital planners, or online courses.

Offer Freelance Services

Use Upwork, Fiverr, or TaskRabbit to offer services like writing, graphic design, or handyman work.

Teach a skill (e.g., music, yoga, coding) through local classes or online platforms.

Rent Out Your Assets

List an extra room on Airbnb or rent out your car on Turo.

Rent out tools, sports equipment, or photography gear via Fat Llama.

Example: Lisa started selling handmade jewelry on Etsy as a side project. Within a year, she earned $5,000 while working on her hobby in her free time.

Conclusion

Saving money on a tight budget isn’t about cutting corners—it’s about making your money work smarter for you. Each of these ten strategies helps you maximize your resources, reduce unnecessary expenses, and build long-term financial security without feeling restricted.

By leveraging free community resources, you can access essential services at no cost. Learning DIY skills allows you to save on home repairs, clothing, and cooking while gaining independence. Buying secondhand and swapping items keeps quality products in your hands for a fraction of the price. Mastering negotiation helps you cut down monthly expenses effortlessly, while free entertainment options allow you to enjoy life without breaking the bank.

Beyond spending wisely, financial freedom also comes from eliminating hidden fees, optimizing food costs, and bartering for services. Conserving energy and water not only lowers your bills but also benefits the environment. Finally, monetizing your hobbies allows you to increase your income while doing what you love, proving that financial stability isn’t just about saving—it’s also about earning smarter.

Small Steps Lead to Big Savings

Each dollar saved is a step toward financial independence. When you implement just a few of these strategies, you’ll start to see a difference in your monthly budget. Over time, these small changes can lead to thousands of dollars in savings per year, giving you more control over your finances and peace of mind.

Take Action Today

Financial security isn’t reserved for the wealthy—it’s built through consistent, mindful choices. Whether you start by negotiating a bill, reducing food waste, or selling a skill online, every action contributes to a more secure financial future.

Which of these strategies will you apply first? Start today, and watch your savings grow! 🚀

Are you constantly struggling with money despite having a budget? You’re not alone! Many people unknowingly make budgeting mistakes that keep them stuck in a cycle of financial stress. The good news? These mistakes are 100% avoidable—and once you fix them, you’ll be on the fast track to getting out of debt and finally taking control of your money.

The fastest way to turn your financial situation around? Get the ultimate guide that teaches you exactly how to organize your budget and eliminate debt! Grab your copy here 👉 Click to Get Your Budgeting Blueprint Now!

If you don’t track your spending, you’ll never know where your money is going. Little expenses add up, leading to budget shortfalls and financial stress. Studies show that people who actively track their expenses save up to 30% more than those who don’t.

How to Fix It

Use a Budgeting App

Leverage technology to monitor your finances effortlessly. Here are some reputable budgeting apps:

YNAB (You Need A Budget): Uses a zero-based budgeting system to ensure every dollar is accounted for, helping you plan ahead and make informed financial decisions.

Mint: A free app that connects to your bank accounts, categorizes transactions, and provides insights into your spending habits. It also offers bill reminders and credit score monitoring.

Goodbudget: Based on the envelope budgeting method, this app helps you allocate funds for different spending categories and manage your finances proactively.

Maintain a Spending Journal

If you prefer a manual approach, record every expense in a notebook or a digital document. Reviewing your spending patterns weekly can highlight areas where you can cut back.

Set Spending Limits

Establish clear budgets for different expense categories such as groceries, entertainment, and transportation. Regularly reviewing these limits ensures you stay on track and make adjustments as needed.

Example: Imagine you grab a $5 coffee every morning before work. That’s $25 a week, or $1,300 a year! Instead, if you make coffee at home, you could save over $1,000 annually—enough to kickstart an emergency fund or invest in your future.

Without an emergency fund, unexpected expenses (medical bills, car repairs) can destroy your budget and lead to debt. The average unexpected expense costs $1,400, and without savings, many people turn to credit cards with high-interest rates.

How to Fix It

Start Small, Then Build Up

Begin with $500-$1,000 as a starter emergency fund.

Gradually increase it to cover 3-6 months of essential living expenses.

Open a Dedicated Emergency Savings Account

Use a high-yield savings account to keep your funds accessible yet separate from daily spending.

Automate monthly deposits to build your emergency fund effortlessly.

Example: Sarah was doing well financially, but when her car unexpectedly broke down, she had no savings and had to rely on a high-interest credit card. If she had an emergency fund, she could have covered the repair without going into debt.

🚀 Struggling to build an emergency fund? The budgeting blueprint shows you EXACTLY how!Start saving today!

Mistake #3: Setting Unrealistic Budgets

Why This Mistake is Costing You Money

Many people set unrealistic budgets that are either too strict or too vague. A budget that’s too restrictive can lead to frustration and burnout, while a budget without clear structure can result in overspending.

How to Fix It

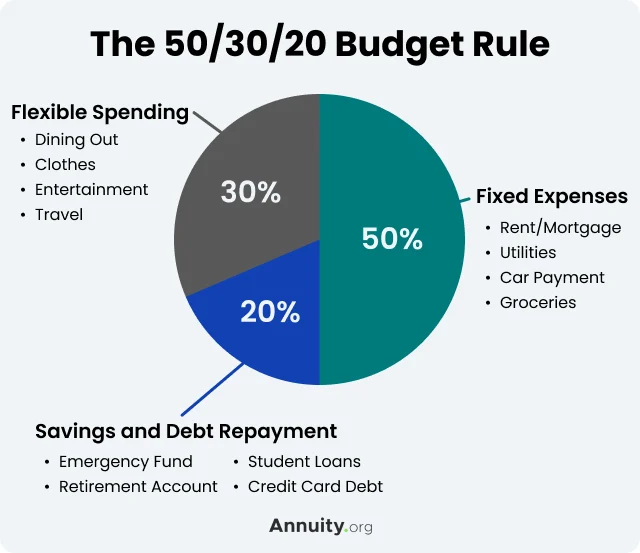

Use the 50/30/20 Rule

A well-balanced budget should account for:

50% of income for necessities (rent, food, bills).

30% for discretionary spending (entertainment, dining out, hobbies).

20% for savings and debt repayment.

Be Flexible & Adjust as Needed

Your budget should evolve with your financial situation. Reassess it monthly to make sure it reflects any changes in income, expenses, or goals.

Example: Emma created an overly strict budget, cutting all entertainment spending. After a month, she felt frustrated and started overspending. Instead, she adjusted her budget to allow for a reasonable entertainment fund, which made it easier to stick to long term.

Mistake #4: Relying on Credit Cards for Everyday Expenses

Why This Mistake is Costing You Money

Using credit cards for daily purchases can lead to high-interest debt, especially if you only pay the minimum balance each month. The average American household carries over $6,000 in credit card debt, with interest piling up rapidly.

How to Fix It

Switch to a Debit or Cash System

Use cash for small, everyday expenses to stay within budget.

Utilize a debit card for essentials instead of relying on credit.

Pay Off Balances in Full

Avoid interest charges by paying off your credit card in full each month. Set up automatic payments to stay on track.

Example: Mike used his credit card for groceries and gas but didn’t pay off his full balance each month. Over a year, he accumulated $800 in interest fees. Switching to a debit card for essentials helped him stay debt-free.

Mistake #5: Forgetting to Adjust Your Budget

Why This Mistake is Costing You Money

Life circumstances change—raises, unexpected expenses, and new financial goals should all prompt budget adjustments. Sticking to an outdated budget can cause unnecessary financial strain.

How to Fix It

Review Your Budget Regularly

Set a monthly budget check-in to evaluate spending and make necessary adjustments.

Reallocate funds based on changing priorities, such as higher savings contributions after a raise.

Account for Seasonal Expenses

Certain months bring extra expenses, like holiday shopping, vacations, or back-to-school costs. Planning ahead prevents financial surprises.

Example: Sarah got a 10% raise but didn’t adjust her budget. Instead of saving more, she unknowingly spent the extra income. After revising her budget, she allocated the raise toward her emergency fund and investment account.

Mistake #6: Overspending on Small Daily Purchases

Why This Mistake is Costing You Money

Many people underestimate the impact of small daily expenses. While a few dollars here and there may seem insignificant, they can add up to thousands of dollars per year, leaving you with less money for savings, investments, or debt repayment.

How to Fix It

Identify Unnecessary Daily Expenses

Track all small purchases for one month to see where your money is going.

Instead of cutting everything, allocate a small, fixed amount for discretionary spending. This prevents impulse purchases while allowing some flexibility.

Example: John used to buy a $10 lunch every workday, spending $200 per month. He started meal prepping at home, cutting his lunch budget to $50 per month—saving $1,800 per year without sacrificing his favorite meals.

Without clear financial goals, you’re more likely to spend aimlessly rather than build wealth. A lack of direction leads to poor financial decisions and delayed financial independence.

How to Fix It

Set SMART Financial Goals

Your goals should be:

Specific – Define exactly what you want (e.g., “Save $10,000 for a house down payment in 12 months”).

Measurable – Track progress over time.

Achievable – Set realistic expectations based on income.

Relevant – Align your goals with your overall financial plan.

Time-bound – Have a clear deadline.

Automate Your Savings

Once you set your goal, make it effortless by setting up automatic transfers to a dedicated savings account.

Example: Emily wanted to build an emergency fund of $5,000 but never got around to saving. She set up an automatic transfer of $200 per month, and within two years, she hit her goal without even thinking about it.

Budgeting isn’t about depriving yourself—it’s about giving yourself more freedom over your money. By avoiding these common mistakes, you set yourself up for financial security, peace of mind, and the ability to enjoy life without constant financial stress.

Here’s what to take away from this guide:

Tracking your spending helps you identify where your money goes, so you can cut waste and spend smarter.

Setting realistic budgets makes it easier to stick with long-term, reducing financial frustration.

Emergency funds prevent financial disasters, saving you from falling into debt during unexpected events.

Credit cards should work for you, not against you—using them wisely avoids costly interest payments.

Your budget should evolve with your life—flexibility is key to staying on track.

Every small expense adds up—but with intentional spending, you can redirect money toward your goals.

Clear financial goals help you build wealth faster—the more specific, the better.

Taking control of your budget doesn’t have to be overwhelming. With the right tools and strategies, you can start making smarter money moves today. If you want a step-by-step plan to master your finances, check out this comprehensive budgeting guide. It provides actionable steps to help you fix budgeting mistakes, eliminate debt, and finally feel confident about your financial future.

Your financial journey starts now. Take that first step toward stress-free finances today!

Leave a Reply